There’s talk of China essentially colonising Cambodia economically, which could lead to physical “colonisation” as more Chinese people are expected to settle in Cambodia in the coming years. What does this mean for the Cambodian culture and economy?

This is the latest headline concern about Chinese people settling in the Asean zone. Indonesia has had persistent concerns about Chinese workers, but this is perhaps more about jobs.

Cambodia has the $3.8 billion Koh Kong port/airport/city project on 45,000 hectares (0.25% of the land area), with a significant 20% of the country’s coastline [with an expected capacity of 10 million tourists a year]. There are questions about [this and] several [other] large-footprint China-related projects. In relatively low-population Cambodia, a more transparent policy discussion could allay concerns about the size of these projects and potential migrant workers and longer-term migrants. But it is not Cambodia alone.

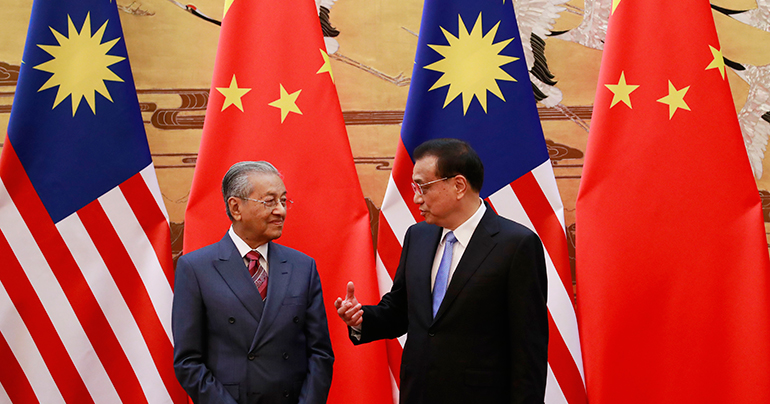

In Malaysia, Prime Minister Mahathir Mohamad has openly worried about the prospect of 700,000 long-term Chinese residents in Country Garden’s $100 billion Forest City mega-development project in Johor, close to Singapore. The recent surprise was his “not for foreigners” statement about this 1,740-hectare project on four reclaimed islands. That population will take 25 years to build up and the population estimate seems overstated; but it represents 15% of Johor’s recent population.

Malaysian federal and state officials have taken pains to explain that Malaysia is open for investment, including in real estate, and that those meeting the long-term stay permit criteria will get it. This walked back Mahathir’s declaration, but he then repeated his “no permits for foreigners” view. I think we are in for more public domestic discussion on this topic in Malaysia and elsewhere.

What are the positives and negatives of China’s Belt and Road Initiative?

China’s BRI energises infrastructure development plans and funding in key countries with railway, port, industrial zones, power generation (coal, hydro, solar) and electricity transmission, expressways, airports and slum upgrading.

Any development project is in the public interest so long as it is properly priced and not caught up by corruption and wastage. Its economic multipliers plus rationale must be proven. Ultimately, bringing good economic development to poorer countries will help establish the roots of progressive politics. The real challenge for the ruling elite is to embrace the idea that they too must learn to share power as the country develops economically. The key is an understanding that corruption is unacceptable. It seems the China-host interactions are often determined by a just a few people. If this is more widely done, it may take a bit longer at the outset, but it might save greater uncertainty later. There has not been much of a Beijing template for its overseas megaprojects. But especially since late 2016, there seems to be more centralised concern and control about what its economic agents are doing overseas.

What is China’s end goal for Belt and Road? What might those countries look like in 10 years that are the largest recipients of Chinese investment?

Much of it relates to boosting the three T’s: tourism, transport and trade. The latest television advertisements feature the “Iron Silk Road” and also the “Information Silk Road”. It helps to export excess capacity from China, benefit from other country of origins for trade, and gain consumption markets and influence in the region. There have been purchases of China military equipment, and there’s even a common expectation that the port-related projects have the capacity to receive naval ship calls. The China-backed Asia Infrastructure Investment Bank and its state-owned enterprises and banks are major players in advancing the projects with host-countries’ private sector or government-linked corporations, and this is regularly done with a government-to-government overlay.

The top ten BRI projects in Asia (by value) are hosted by Malaysia (with numbers one to three by value), Pakistan (numbers four to five), Myanmar, Bangladesh, Laos, Thailand and Indonesia. China states its hope to help bring peace, stability, development and prosperity to the region.

In the coming years, we should be using Huawei phones and its mobile networks, using eWallets and saving funds at Ant Financial alongside the usual Western options. Alibaba and its logistics business should be big in the region. I hope to visit Laos in 2020 to get on its new high-speed rail to get to Kunming and then Shanghai. But by 2028, it does not look like Bangkok-to-Vientiane will be ready.

In 2017, China provided 30% of Cambodia’s investment capital, which no longer enjoys funding from the EU or the US. What does this mean for human rights in Cambodia?

In general, China has been a relative latecomer to the FDI [foreign direct investment] scene. So, on a cumulative basis, traditional investors like the EU countries and US would still be bigger than China in many countries. China has done particularly well on trade integration with its neighbours. Not surprisingly, it comes up tops on the trade front for many Asian countries, and it has also been very successful in winning engineering, procurement and construction (EPC) projects for apartments, dams, roads and more. The third wave has been the advent of China investment capital and loans for mega-projects.

Asians have been rankled by Western investments (and even trade) coming with conditions about human rights and sustainability. Under China’s rising hegemony, it seems that it is up to domestic political players to contest such issues. Of course, opposition politicians may find it tough going, as China (and other countries) will always be respectful of whoever leads the country. In the case of Malaysia, after the electoral defeat of the long-ruling Barisan Nasional coalition, China was no less respectful of its new leader and vice versa.

Malaysia recently pulled out of several large Chinese-funded infrastructure projects. Was that a wise move?

Malaysia’s request to renegotiate about $22 billion in contracts with China has been eye catching; these are for the East Coast Rail Link and some previously unknown (non-BRI) oil and gas pipeline deals. In the context of Asia BRI projects, Malaysia really stands out, as it has the top three projects: East Coast Rail Link, Melaka Gateway and the Kuantan port and industrial zone. These total over $30 billion.

Mahathir pushes for contract renegotiation with China’s understanding of Malaysia’s tricky debt situation. It seems more to cut cost than to cancel. Malaysia has said that China may have been misled by “our fellows” on the high-priced deals. Laos specialists say the same about the initial cost of their high-speed rail project. This has been nearly halved to be more affordable, and the China-Laos SOE joint venture has about 30% construction progress now.

Vietnam recently saw street protests against special economic zones seen as favouring China by essentially selling it pieces of Vietnam. Should citizens be concerned by such deals? If so, why, and how can they fight back?

Vietnam’s legislature appears to have delayed to May 2019 a bill to allow foreign investors the use of special economic zones. Hanoi seems cautious about preferential loans from China for infrastructure development and its development aid. This seems consistent for its state-level approach. Vietnam has not been part of the biggest BRI projects in the region. If you look at the list of top 25 projects, there is nothing involving Vietnam. In fact, those active in business there point out that Vietnam is getting closer to Russia strategically. But it is a different story at the private-sector level, with active private business with China and a move to settling deals in the Chinese yuan. It seems the Vietnamese are welcoming of regular trade and business but more sensitive if it comes with levers of control. The China-Vietnam relationship is trickier than others. Close neighbours with a long history tend to be more touchy and cautious.

What risks are there to China’s Belt and Road Initiative if Southeast Asian nations such as Malaysia and Myanmar continue to terminate or drastically reduce Chinese projects? What impact could this have on China’s banking and finance sectors?

Malaysia’s concern on high-debt China projects was a topic of political campaigning for its 14th General Election in May 2018. The then political opposition pointed to the problematic news about Sri Lanka’s port project in its speeches to urban and rural crowds. In our own research, we found in the rural Malay heartland of Pahang (former PM Najib’s home state) concern about China projects. A middle-aged lady told us that she welcomed investment but not debt. Perhaps this is not a surprise, as many Malaysians have high household debt and they can understand the issue.

Malaysia is now under the Pakatan Harapan administration led by Mahathir. He has been a long-time friend of China, but he and others worry that Malaysia cannot afford the high-debt high-cost projects signed under the Najib administration. After that, there was news of Myanmar wanting to downsize its $7.3 billion Kyauk Pyu deepwater port (the sixth-ranked project for Asia BRI) to a “more plausible” $1.3 billion according to its economic adviser. They are still figuring this out, and the industrial park portion has yet to be addressed. Myanmar also has projects with India, an Italian-Thai consortium and others.

The Malaysia and Myanmar cases are just at the start of a negotiation process. Time will tell, but the impact on China’s banking and finance will likely be limited, as there are likely also other interesting deals to come for FDI and in the digital-ecommerce sector as well as Chinese yuan settlement.

To what extent do you believe Southeast Asian nations are becoming more cautious about the types of BRI infrastructure projects they partner with China on? Do you believe this caution is merited, or is there a possibility that some nations may overcorrect and miss out on much-needed investment?

As we enter a more cautious global trade situation under the US-led trade war gambit, it is an opportunity and risk for BRI and China. Debt and worries about debt have been mounting. Emerging market currencies have been correcting. Rising caution is expected all around.

With China under pressure to forge alliances with regimes friendly to Chinese investment, what likelihood do you see of China being more assertive in throwing its support behind political parties that would welcome closer ties to the superpower?

China will be figuring out that there can be political change and shifts despite the apparent economic boost from economic deals. As economic risk appetite takes a breather, it is likely political risk has to adjust too. There seems need for careful political judgment and a more nuanced and balanced approach to widen stakeholder support for BRI and other projects. The Najib-Malaysia case shows how a strongman turned out to be a strawman.

Asean populations are suddenly exposed to the world of social media. For instance, we can watch Facebook videos of local workers complaining about labour issues at a China-owned steel plant in Kuantan, Pahang! China has provided cheap handsets and helped roll out 4G high-speed mobile networks, including to many rural areas. The political transition in Malaysia is partly driven by this. So it is increasingly about handling wider public opinion and multiple stakeholders and not just about supporting particular political parties or regimes.

Khor Yu Leng is an independent political economist and an expert on Chinese investment at Segi Enam Advisors and a research associate at the Institute of China Studies at the University of Malaya.